Are you dealing with unpaid medical bills? If yes, we understand how stressful it can be, and the fear of wage garnishment can make the situation even worse.

Have you ever thought, can medical debt collectors garnish wages? Well, the answer depends on specific legal and financial factors, including wage garnishment laws and court involvement.

To protect your income and maintain financial stability, you need to understand your wage garnishment rights. Knowing how the debt collection process works and looking for legal debt solutions can help you avoid medical debt garnishment.

In this blog, we will break down everything you need to know, from medical debt protection strategies to court-ordered wage garnishment, so you can be ready and take the right steps to protect your money.

Latest Facts and News About Medical Debt Garnishment

Before we look into the legal side of wage garnishment, it helps to understand how common and serious medical debt has become in the U.S. today.

- Rising medical debt: Medical debt affects millions of Americans annually. It is the largest type of debt in collection, with around 100 million Americans dealing with it. Even larger than most debt from credit cards, utilities, and auto loans. A 2025 study showed that around 9% of Americans owe more than $250 for healthcare costs.

- Policy updates: In January 2025, the Consumer Financial Protection Bureau (CFPB) announced a rule that removes $49 billion in unpaid medical bills from credit reports. States have leveraged American Rescue Plan funds to clear over $1 billion in medical debt for 750,000 people. By 2026, these efforts will help eliminate up to $7 billion in debt for nearly 3 million people.

- Consumer protection laws: The Fair Debt Collection Practices Act (FDCPA) protects consumers from abusive and unfair collection practices. In addition, recent regulations by the Consumer Financial Protection Bureau (CFPB) removed medical bills under $500 or less than a year old from credit reports.

What Is Wage Garnishment?

Wage garnishment is a legal process where a court orders the employer to take a portion of your wages to pay off a debt. This money is sent to the creditor directly until the debt is paid in full.

The wage garnishment process

If your medical debt ends up in court, here’s what the legal journey typically looks like:

- Court judgment: The garnishment process begins when a creditor sues a debtor. If the creditor wins the case, the court will require the debtor to pay up.

- Garnishment order: After this judgment, the court sends the garnishment order to the debtor’s employer or bank, specifying the amounts to be deducted.

- Employer compliance: Upon receiving the notice, the employer deducts the garnished portion from the debtor’s paycheck and sends it to the creditor.

- Notification: You’ll be informed about the garnishment, including the amount to be deducted and the creditor’s details.

- Duration: This garnishment continues until the debt is fully paid or if the debtor challenges or changes the repayment terms.

Common reasons for wage garnishment

Wage garnishment can happen due to different types of debts. Here are the common reasons:

| Reason for Wage Garnishment | Explanation |

| Medical Debt | If you fail to pay your medical bills, they can sue you, and if they win, they may garnish your wages to pay off the debt. |

| Credit Card Debt | If you don’t pay your credit card bills, a court may order wage garnishment to collect the debt. |

| Unpaid Taxes | If you owe unpaid taxes, federal or state agencies may garnish your wages, often without a court order. |

| Student Loans | Federal student loans that are not being paid can be garnished from wages without a court order from the government. |

| Struggling with any of the above wage garnishments and need a solution fast? Watch this quick YouTube video to learn How To End Your Wage Garnishment For Good. |

Legal process for medical debt garnishment

While various debts can lead to wage garnishment, medical debt follows a specific legal process:

Steps involved in garnishment for medical debt

If you fall behind on medical bills, creditors can eventually take legal steps to collect them. Wage garnishment is one of them, but it doesn’t start there. Here’s how the process usually comes out:

- A lawsuit

A hospital, clinic, or collection agency must file a lawsuit in civil court to recover what’s owed. They’ll need to show records of your bill, the amount due, and any previous attempts to collect. If you don’t respond to the court notice, the creditor usually wins by default.

- Judgment

If the court sides with the creditor, the creditor can issue a judgment that officially states you owe the money. This step is tough; it gives the creditor legal permission to move forward with collection. You’ll be notified, and depending on your state, you may still have time to contest it.

- Garnishment order

With a judgment in hand, the creditor can ask the court to send a garnishment order to your employer. This order tells them to take a set portion of your paycheck and send it directly to the creditor each pay period.

- Justification

Just because there’s an order doesn’t mean you’re out of options. In many states, you can request a hearing to justify your side; maybe the debt is wrong, or your income is legally protected. These hearings usually need to be requested quickly, sometimes within a week or two.

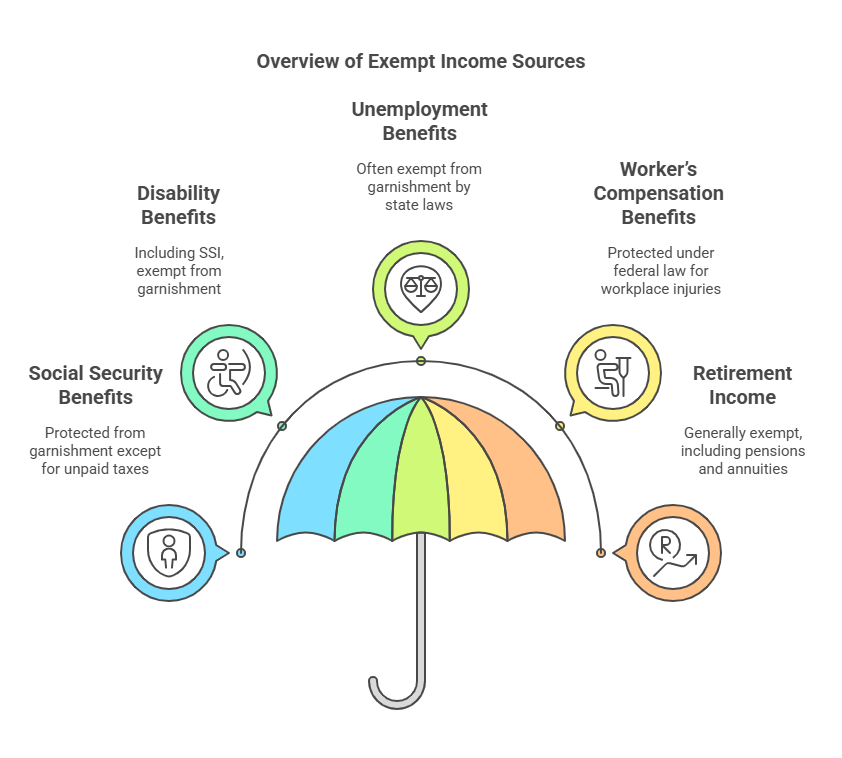

Exemptions and protections

Here are some exemptions under federal law:

How to prevent wage garnishment for medical debt?

Proactive steps can help you avoid wage garnishment for medical debt, saving you from financial strain and legal complications.

Here are steps you can take to prevent medical debt garnishment:

Payment plans and negotiations

Talk directly to your healthcare provider or debt collector to negotiate a payment plan and avoid wage garnishment. Here is how you can do it:

- Assess your financial situation before contacting your creditor. Determine the total amount you owe in debt and how much you can afford.

- Reach out to your creditor when it is difficult to make a payment. Be honest and explain your situation. Many creditors prefer to negotiate and find a solution.

- Suggest a way to solve the problem. Offer a solution based on your situation that works for both you and the creditor. For example, if you have saved up some money and you do not have the entire amount, offer to make one payment with what you have. You can also suggest a monthly payment plan according to how much you can afford.

- Make sure to keep records of everything you communicate with the creditor. Write down the dates and the details of any agreements and payment plans made. This can be really helpful if any issues may arise later.

Legal assistance and debt relief programs

The other option is to get legal help or choose a debt relief program:

- Talk to a debt relief lawyer for guidance and legal support.

- You can apply for a debt relief program through non-profit agencies that help with medical debt.

- A non-profit credit counseling agency assists you with your budgeting, repayment strategy, and negotiation with creditors on your behalf.

- A consumer proposal lets you offer to pay less than what you owe and can stop wage garnishment immediately. It involves extending an offer to creditors to settle out of court under the Bankruptcy and Insolvency Act.

- Bankruptcy as a last resort, If medical debt becomes unmanageable, bankruptcy may stop wage garnishment. Chapter 7 can erase most medical bills, while Chapter 13 lets you repay over time. It affects your credit, so speak with a bankruptcy attorney first.

Let Hall’s IRS be Your Guide to Save You from Wage Garnishment → Book an Appointment Now!

Federal and state wage garnishment laws

Certain federal and state provisions exist that shield one from wage garnishment.

Federal limits

A salary garnishment cannot exceed the figure permitted under the Consumer Credit Protection Act (CCPA). That is, an individual’s salary will be garnished only to a maximum of either 25% of disposable earnings or the amount by which disposable earnings exceed 30 times the federal minimum wage, whichever is less.

The federal minimum wage remains $7.25/hour in 2025, meaning garnishment cannot occur if your weekly disposable earnings are $217.50 or less.

Likewise, the Fair Debt Collection Practices Act (FDCPA) also protects an individual from debt collectors using abusive and deceptive strategies while attempting to collect the debt.

State rules

Laws protecting an individual from garnishment vary from state to state.

For example, in Arkansas, wage garnishment would apply according to federal rules, except for laborers and mechanics, who will have additional protections.

In California, the garnishment is the smaller of 25% of your disposable earnings or the amount that your earnings exceed 40 times the state’s minimum wage.

Conversely, Delaware allows 15% of disposable earnings to be garnished, compared to the federal maximum of 25%.

Consequences of ignoring medical debt

Ignoring medical debt won’t affect your financial health. Thus, it is important to know about the issues to address them in the appropriate avenues.

- Damaged credit scores: Ignoring medical debt lowers your credit score because healthcare providers can send the debt to collection agencies, who will then report it to credit bureaus as if a medical bill is unpaid by you. This makes it hard for you to acquire loans or rent a house.

- Increased interest rates: Your interest rates and late fees can increase the amount you owe if you do not pay your medical bills on time.

- Legal consequences: Creditors can take legal action if you don’t pay your medical debt. This may include a lawsuit or wage garnishment.

- Restricted access to future healthcare: Some providers may refuse future non-emergency care or send unpaid bills to collections if old debts remain unresolved.

Take control of your finances with Hall’s IRS

Medical debt collectors can garnish your wages only after a lawsuit and court order. And if managing debt feels stressful to you, a tax or legal expert can guide you through your options and protect your income. That’s where Hall’s IRS makes the difference.

We don’t just explain your rights; we help you fight for them. Our experts review your case in detail and personalize our service approach.

Wondering how else we can help?

- We contact collectors, challenge unfair claims, and negotiate on your behalf.

- If there’s a judgment against you, we’ll explore every legal option to reduce or dismiss it.

- If you’re behind on payments, we can create realistic repayment plans that protect your paycheck.

With Hall’s IRS, you get relief.

Let us help you keep what you’ve earned. Contact Hall’s IRS today to get the help you deserve.

FAQ's

No, medical debt collectors can not take money from your wages unless they’ve first gotten a court order. They need to file a lawsuit against you in court, win the case, and get a judgment before they can get an order for garnishment.

Under federal law, the amount that a medical debt can be taken from your wages does not exceed 25% of your disposable earnings or what your disposable earnings are above 30 times that of the federal minimum wage, whichever is smaller. If your weekly disposable income is $217.50 or less, they cannot garnish your wages.

Some wages or income sources are protected against wage garnishment, such as Social Security benefits, disability benefits, Supplemental Security Income (SSI), unemployment income, workers’ compensation benefits, and retirement income or annuities.

Yes, you can negotiate with debt collectors regarding the medical debts you have to avoid garnishment. Many creditors prefer payment plans or settlements instead of taking legal action. You can contact them, explain your situation, and suggest a realistic repayment plan.

Federal laws protect workers who are facing wage garnishment. These laws include limits on how much wages can be garnished and exempt some incomes from garnishment. The Fair Debt Collection Practices Act (FDCPA) also stops debt collectors from being abusive or unfair.

{kind=link}

{kind=link}